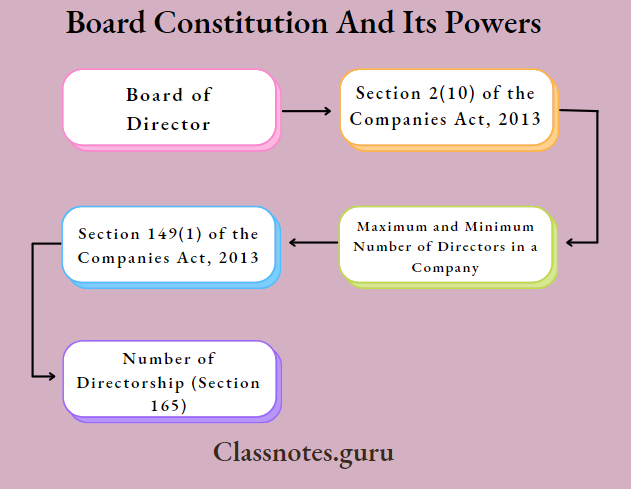

Board Constitution And Its Powers

Board of Director

Section 2(10) of the Companies Act, 2013 defines that “Board of Directors” or “Board”, about a company, means the elective body of the directors of the company.

The term ‘Board of Directors’ means a body duly constituted to direct, control, and supervise the affairs of a company.

Maximum and Minimum Number of Directors in a Company

Section 149(1) of the Companies Act, 2013 requires that every company shall have a minimum number of 3 directors in the case of a public company, two directors in the case of a private company, and one director in the case of a One Person Company. A company can appoint a maximum of 15 fifteen directors without any specific compliance. A company may appoint more than fifteen directors after passing a special resolution in a general meeting.

The restriction of a maximum number of directors shall not apply to Section 8 companies.

Number of Directorship (Section 165)

The maximum number of directorships, including any alternate directorship, a person can hold is 20. Same time, a person cannot be a director of more than 10 public companies. To count such directorship in public companies, directorship in private companies that are either holding or subsidiary of a public company shall be included.

Alternate directorship shall also be included while calculating the directorship of 20 companies. Section 8 companies will not be counted for the maximum number of directors. Further, the members of a company may restrict the abovementioned limit by passing a special resolution for its directors.

Power of Board

- To make calls on shareholders in respect of money unpaid on their shares;

- To authorize the buy-back of securities under section 68;

- To issue securities, including debentures, whether in or outside India;

- To borrow money;

- To invest the funds of the company;

- To grant loans or give guarantee or provide security in respect of loans;

- To approve financial statements and the Board’s report;

- To diversify the business of the company;

- To approve amalgamation, merger, or reconstruction;

- To take over a company or acquire a controlling or substantial stake in another company;

- To make political contributions;

- To appoint or remove key managerial personnel (KMP);

- To appoint internal auditors and secretarial auditors;

Contributions to Charitable Funds and Political Parties

The power of contributing to ‘bona fide’ charitable and other funds is available to the board subject to certain limits.

Further, the prior permission of the company in a general meeting is required if such contribution exceeds five percent of its average net profits for the three immediately preceding previous years.

Board Constitution Under Companies Act 2013

Prohibitions and Restrictions Regarding Political Contributions

Notwithstanding anything contained in any other provision of this Act, a company, other than a Government company and a company which has been in existence for less than three financial years.

Audit Committee

Every Listed Public Company and (i) all public companies with a paid-up capital of ten crore rupees or more;

All public companies having turnover of one hundred crore rupees or more; (iii) all public companies, having in aggregate, outstanding loans or borrowings or debentures or deposits exceeding fifty crore rupees or more shall form an Audit Committee comprised of a minimum 3 directors with a majority of the Independent Directors and majority of members of the committee shall be a person with the ability to read and understand financial statement.

Nomination and Remuneration Committee

Every listed company and (i) all public companies with a paid-up capital of ten crore rupees or more; (ii) all public companies having turnover of one hundred crore rupees or more; (iii) all public companies, having in aggregate, outstanding loans or borrowings or debentures or deposits exceeding fifty crore rupees or more.

The committee shall consist of three or more non-executive directors out of which not less than one-half shall be independent directors, shall constitute the Nomination and Remuneration Committee consisting of three or more non-executive directors out of which not less than one-half shall be independent directors.

The Stake-holders Relationship Committee

Section 178(5) of the Companies Act, 2013 provides for the constitution of the stakeholder’s relationship committee.

The Board of a company that has more than one thousand shareholders, debenture-holders, deposit-holders, and any other security holders at any time during a financial year is required to constitute a Stakeholders Relationship Committee consisting of a chairperson who shall be a non-executive director, and such other members as may be decided by the Board.

Risk Management Committee under SEBI (Listing Obligations and Disclosure Requirement) Regulations, 2015

As per Regulations 21 of the SEBI (Listing Obligations and Disclosure Requirement) Regulations, 2015, the board of directors of the top 100 listed entities, determined based on market capitalization, as at the end of the immediate previous financial year shall constitute a Risk Management Committee. The Board of Directors shall constitute a Risk Management Committee, and the majority of members of the Risk Management Committee shall consist of members of the board of directors. The Chairperson of the Risk management committee shall be a member of the board of directors and senior executives of the listed entity may be members of the committee.

Corporate Social Responsibility Committee

The Section applies to the following classes of companies during any financial year:

- Companies having a Net Worth of 500 crores or more;

- Companies having a turnover of 1,000 crores or more;

- Companies having Net Profit of 5 crores or more.

Other Board Committees

In addition to the Committees of the Board mandated by the Companies Act, 2013 viz, Audit Committee, Nomination and Remuneration Committee, Stakeholders Relationship Committee, and the CSR Committee, the Board of Directors may also constitute other Committees to oversee a specific objective or project. The nomenclature, composition, and role of such Committees will vary, depending upon the specific objectives of the company.

A few examples of such Committees prevalent in the corporate sector in India and abroad are given below:

- Corporate Governance Committee

- Science, Technology and Sustainability Committee

- Regulatory, Compliance, and Government Affairs Committee.

- Investment Committee

- Ethics Committee.

Section 154 of the Finance Act, 2017 amends Section 182 of the Companies Act, 2013. As per the amendment, the limit on the maximum amount that can be contributed by a company to a political party has been removed.

Powers Of Board Of Directors In Company Law

Board Constitution And Its Powers Descriptive Questions

Question 1. Can the Board of directors of a company delegate any of its powers to others? Discuss.

Answer:

Powers of Board Section 179

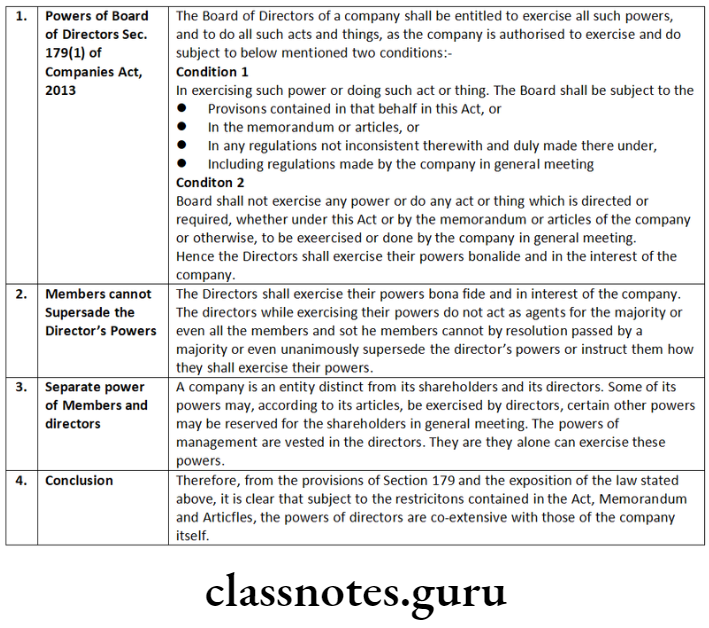

- Section 179 of the Act deals with the powers of the board; all powers to do such acts and things for which the company is authorized are vested with the board of directors. But the board can act or do the things for which powers are vested with them and not with general meetings.

Powers that can be excised with Board Resolution only. [Section 179(3] read with Rule 8 of Companies Meetings of Board and its Powers Rules 2014

The following powers of the Board of Directors shall be exercised only using resolutions passed at meetings of the Board, namely:

- To make calls on shareholders in respect of money unpaid on their shares;

- To authorize buy-back of securities under Section 68;

- To issue securities, including debentures, whether in or outside India;

- To borrow money;

- To invest the funds of the company;

- To grant loans or give guarantee or provide security in respect of loans;

- To approve financial statements and the Board’s report;

- To diversify the business of the company;

- To approve amalgamation, merger, or reconstruction;

- To take over a company or acquire a controlling or substantial stake in another company;

- To make political contributions;

- To appoint or remove key managerial personnel (KMP);

- To take note of appointment(s) or removal(s) of one level below the Key Management Personnel;

- To appoint internal auditors and secretarial auditors;

- To take note of the disclosure of the director’s interest and shareholding;

- To buy, and sell investments held by the company (other than trade investments), constituting five percent or more of the paid-up share capital and free reserves of the investee company;

- To invite accept or renew public deposits and related matters;

- To review or change the terms and conditions of public deposit;

- To approve quarterly, half-yearly, and annual financial statements or financial results as the case may be.

- To appoint internal auditors and secretarial auditors.

Delegation of Powers to Directors, MD, Manager, etc.

Board may, by a resolution passed at a meeting, delegate

- To any committee of directors,

- The managing director,

- The manager or

- Any other principal officer of the company or

- In the case of a branch office of the company, the principal officer of the branch office, the powers specified in clauses (d) to (f) on such conditions as it may specify.

Cs Company Law Board Powers Questions

Question 2. Explain the prohibitions and restrictions regarding political contributions by a company.

Answer:

Question 3. Comment on the following:

The powers of the directors of a company are co-extensive with those of the company.

Answer:

Question 4. Explain the provisions of the Companies Act, 2013 relating to the constitution of an audit committee. What role does the audit committee play in the management of a company?

Answer:

Audit Committee Sec.177 of Companies Act, 2013

Companies, required to have Audit Committees

The requirement of the constitution. of Audit Committee has been limited to:

- Every listed Public Companies; or

- The following class of companies –

- All public companies with a paid-up capital of ten crore rupees or more;

- All public companies having a turnover of one hundred crore rupees or more;

- All public companies, having in aggregate, outstanding loans borrowings debentures, or deposits exceeding fifty crore rupees or more.

Amended by Companies Act, 2017: In Section 177 of the Companies Act, 2013, in sub-section (1), for the words “every listed company”, the words “every listed public company” shall be substituted;

Composition of Directors

- The Committee shall comprise a of minimum 3 directors with the majority of the directors being Independent Directors. The majority of members of the audit committee including its chairperson shall be persons with the ability to read and understand the financial statement.

Transition Period

- A transition period of one year from the date on which the new Act comes into effect has been provided to enable companies to reconstitute the Audit Committee.

Role of Audit Committee Section 177 (4)

Every Audit Committee shall act by the terms of reference specified in writing by the Board.

Terms of reference as prescribed by the board shall inter alia, include, –

- the recommendation for appointment, remuneration, and terms of appointment of auditors of the company;

- (In the case of Government Companies, in Clause (1) of sub-section (4) of Section 177, for the words “recommendation for appointment, remuneration and terms of appointment” the words “recommendation for remuneration” shall be substituted Exemption Notification dated 05-06-2015)

- review and monitor the auditor’s independence and performance, and the effectiveness of the audit process;

- examination of the financial statements and the auditors’ report thereon;

- approval, or any subsequent modification of transactions of the company with related parties;

- The Audit Committee may make omnibus approval for related party transactions proposed to be entered into by the company subject to such conditions as prescribed under rule 6A of the Companies (Meetings of Board and its Powers) Rules, 2014.

- Further, in case of transactions, other than transactions referred to in Section 188 (Related Party Transactions), and where the Audit Committee does not approve the transaction, it shall make its recommendations to the Board.

- In case any transaction involving any amount not exceeding one crore rupees is entered into by a director or officer of the company without obtaining the approval of the Audit Committee and it is not ratified by the Audit Committee within three months from the date of the transaction, such transaction shall be voidable at the option of the Audit Committee and if the transaction is with the related party to any director or is authorized by any other director, the director concerned shall indemnify the company against any loss incurred by it:

- The provisions of this clause shall not apply to a transaction, other than a transaction referred to in Section 188, between a holding company and its wholly-owned subsidiary company.

- scrutiny of inter-corporate loans and investments;

- valuation of undertakings or assets of the company, wherever it is necessary;

- evaluation of internal financial controls and risk management systems;

- monitoring the end use of funds raised through public offers and related matters.

Board Of Directors Composition And Powers

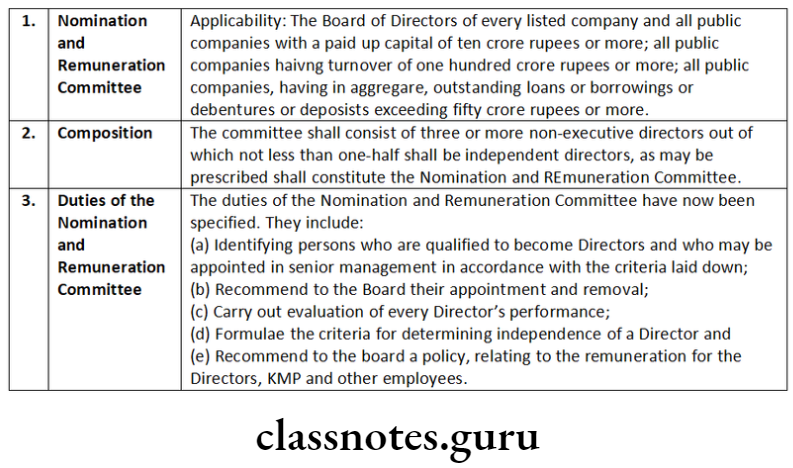

Question 5. Explaining the provisions of the Companies Act, 2013, state the duties of the Nomination and Remuneration Committee.

Answer:

Question 6. State the situations under which a company is required to constitute the Audit Committee.

Answer:

Section 177(1) of the Companies Act, 2013 read with Rule 6 of the Companies (Meeting of the Board and its Powers) Rules. 2014, provides that the Board of directors of the following companies are required to constitute an Audit Committee of the Board –

- Every listed public company;

- All public companies with a paid-up share capital of 10 crore rupees or more;

- All public companies having turnover of 100 crore rupees or more; (iv) All public companies, having in aggregate, outstanding loans or borrowings or debentures or deposits exceeding 50 crore rupees or more.

- The paid-up share capital or turnover or outstanding loans or borrowings or debentures or deposits, as the case may be, as existing on the date of last audited financial statements shall be taken into account for the purpose.

Question 7. The board of directors of Charity Ltd. wants to understand from you the applicability of the provisions relating to CSR to companies including requirements to constitute a CSR committee. Inform the Board.

Answer:

Section 135 of the Companies Act, 2013 about Corporate Social Responsibility specify that:

- every company having a net worth of 500 crore or more;

- every company having a turnover of 1000 crore or more; or

- every company having a net profit of ₹5 crore or more.

During the immediately preceding financial year shall constitute a Corporate Social Responsibility Committee of the Board consisting of 3 or more directors, out of which at least 1 director shall be independent.

Although, where a company is not required to appoint an independent director under Section 149(4) of the Companies Act, 2013, it ‘shall have in its Corporate Social Responsibility Committee 2 or more directors.’

Additionally, as per Rule 5 of the Companies (Corporate Social Responsibility Policy) Rules, 2014, a private company having only 2 directors on its Board shall constitute its CSR Committee with 2 such directors.

Concerning a foreign company covered under these rules, the CSR Committee shall comprise at least 2 persons of which 1 person shall be as specified under clause (d) of section 380(1) of the Companies Act, 2013 and another person shall be nominated by the foreign company. The role of the Corporate Social Responsibility Committee is-

- to formulate and recommend to the Board, a Corporate Social Responsibility Policy which shall indicate the activities to be undertaken by the company in areas or subjects, specified in Schedule VII of the Companies Act, 2013;

- to recommend the amount of expenditure to be incurred on the activities referred to in clause (a) above; and

- to monitor the Corporate Social Responsibility Policy of the company from time to time.

After taking into account the recommendations of the. CSR Committee, the Board shall approve the CSR Policy for the company.

Question 8. Approval of the Audit Committee to a related party transaction can be granted by passing a circular resolution. Discuss.

Answer:

Section 188(1) of the Companies Act, 2013 prohibits the Board from dealing with an item of business about a contract or arrangement with a related party through a circular resolution. However, the law is silent on dealing with any item of business by the Audit Committee through a circular resolution.

- Here, the intention of the Legislature is required to be gathered from the language used; which means that attention should be paid to what has been said as also to what has not been said.

- As a consequence, however, it cannot be added that the law imposes any restriction, the principle applicable to meetings of the Board would apply to the meetings of the Audit Committee too, while dealing with items of business on related party transactions.

- As per the Secretarial Standard on Meetings of the Board of Directors (SS-1), the Audit Committee should discuss related party transactions that are not in the ordinary course of business or which are not on an arm’s length basis at its meetings and not through circulation.

- However, there is no bar on omnibus approval of limits being passed by a circular resolution by the Audit Committee. Space to write important points for revision-

Functions Of Board Under Companies Act

Board Constitution And Its Powers Practical Questions

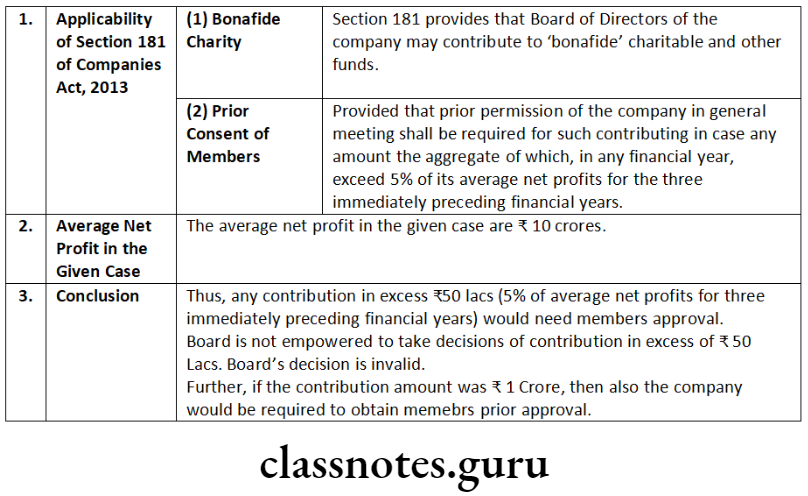

Question 1. Net profits of PQR Ltd. during the following years as disclosed in the statement of profit and loss are as under:

Financial year ended Net profits (in crore)

31st March 2013 10

31st March 2014 12

31st March 2015 08

The Board of Directors of the company at its meeting decided to contribute to a charitable organization, for charitable purposes, a sum of ₹ 3 crores out of the net profits of the financial year ended 31st March 2015. This contribution has been made by the Board without seeking the approval of shareholders in a general meeting.

In light of the provisions of the Companies Act, 2013, examine the validity of the contribution made by the company. What shall be your answer in case the Board decides to contribute 1 crore only?

Answer:

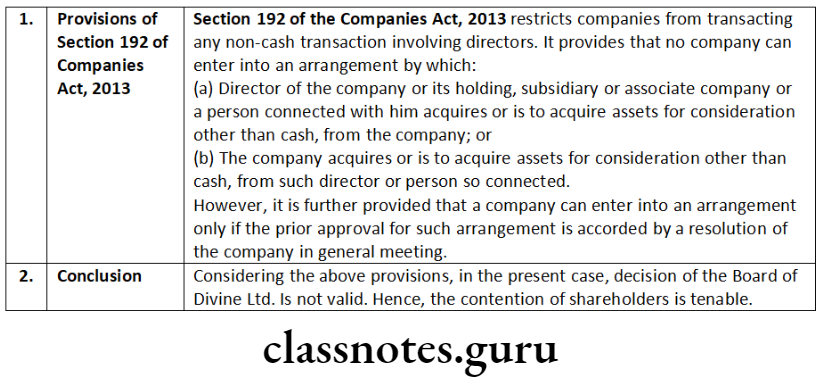

Question 2. The Board of Directors of Divine Ltd. decides to enter into a contract whereby Manish, a director of the company shall acquire certain assets from the company for consideration other than cash, without seeking approval of the company in its general meeting.

Certain shareholders of the company object to the said decision of the Board. Referring to the provisions of the Companies Act, 2013, examine the validity of the Board’s decision and state whether the contention of the shareholders shall be tenable.

Answer:

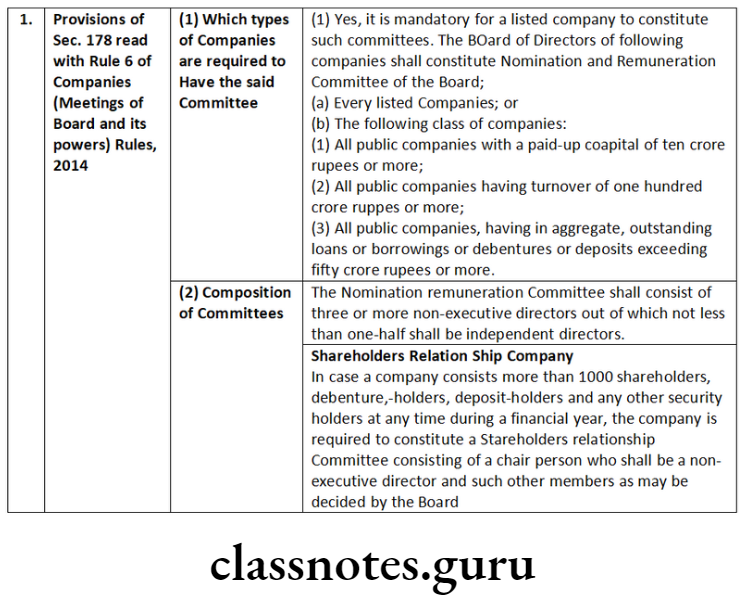

Question 3. Examining the provisions of the Companies Act, 2013, relating to the constitution of a ‘Nomination and Remuneration Committee’ and ‘Stakeholders Relationship Committee’, answer the following:

- Is it mandatory for a listed company to constitute such committees? Also, state whether it is mandatory for a non-listed public company having paid-up share capital of 5 crore to constitute such committees.

- What shall be the composition of the committees in case the company is required to constitute such committees?

Answer:

Question 4. Charjee Biotech Private Limited is a two-year-old company. The Board of Directors of the company wants to contribute 2.8% of its average net profits of the last years to the Prime Minister’s National Relief Fund. Referring to the provisions of the Companies Act, 2013, advise the board.

Answer:

Section 181 of the Companies Act, 2013 states that the Board of Directors of a company may contribute to bona fide charitable and other funds, provided that prior permission of the company in a general meeting shall be required for such contribution in case any amount of the aggregate of which, in any financial year, exceed five percent of its average net profits for the three immediately preceding financial years.

In the given case, Charjee Biotech Private Limited wants to contribute 2.8% of its net profits for the last two years, as it has been in existence for the last two years only.

Prime Minister’s National Relief Fund is a bona fide charitable fund. As the rate of contribution does not exceed 5% of the average net profits, prior permission of members in general meetings is not required. A resolution passed by the Board of Directors shall suffice for making the said contribution.

Board Constitution Under Companies Act 2013

Question 5. The Board of Directors of Wood Ltd. is authorized to borrow money upto 2 crores. The Board of Directors got sanctioned a loan of 30 lakh from a Bank for payment of debt liabilities of the company. But the Board of Directors used this amount towards payment of their traveling and tour expenses. Will Wood Ltd. be held liable for prepayment of the loan? Discuss.

Answer:

In a clear case of V.K.R.S.T Firm v. Oriental Investment Trust Ltd. under the authority of the company, its managing director borrowed large sums of money and misappropriated it. The company was held liable stating that where the borrowing is within the powers of the company, the lender will not be prejudiced simply because its officer has applied the loan to unauthorized activities provided the lender did not know about the intended misuse.

Applying the principles of the above-decided case in the above case Wood Ltd. will be held liable for repayment of the loan of 30 lakhs which is well within the sanctioned limits of the company.

Question 6. The Board of Directors of XYZ Ltd. wants to delegate all or any of their powers to any of the directors of the company or any person even not in the employment of the company for transfer of securities. Referring to the provisions of the Companies Act, 2013 advise in the matter.

Answer:

There is no restriction on the delegation of powers of the Board of Directors of the company except as provided in the first proviso to Section 179(3) of the Companies Act, 2013.

It provides that The Board may delegate power to borrow money, to invest the funds of the company, and to grant loans or give guarantee or provide security in respect of loans, by way of resolution to any committee of directors, the managing director, manager or any other principal officer, or principal officer of a branch of the company.

Apart from this, the Board of Directors may delegate all or any of its powers to any person including a person not in employment of the company if the Articles of Association so provide.

Appropriately, in the given case the Board of Directors of XYZ Ltd. may delegate the powers relating to the transfer of securities only when the Articles of Association allows delegation of the powers to any of the directors of the company or any person not in employment of the company.

DEF Ltd. has made a profit for the last 3 consecutive financial years as under:

Question 7. Considering the provisions of the Companies Act 2013, state whether:

- DEF Ltd. can contribute 33.75 crores directly to a political party by a bearer cheque.

- What is the limit on the maximum amount that can be contributed by a company to a political party?

- Would your answer be different, if DEF Ltd. is a “Government Company” and donation is given by an “account payee cheque”?

Answer:

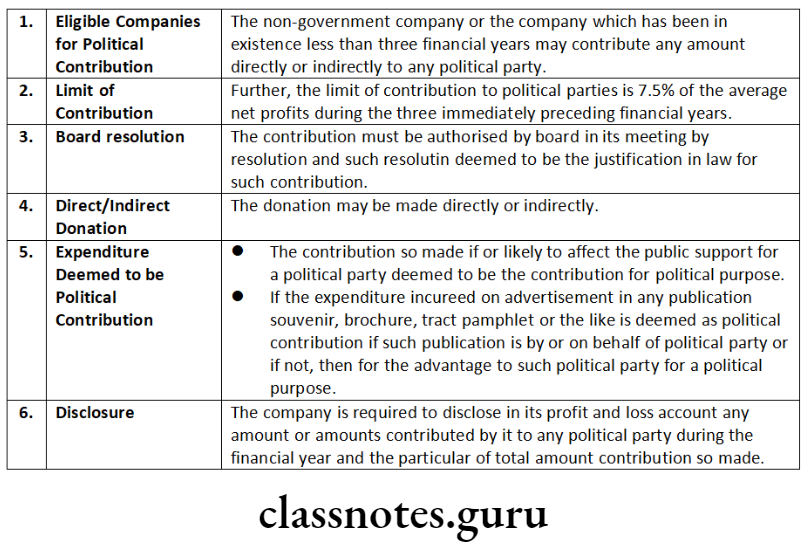

According to Section 182 of the Companies Act, 2013. a company, other than a government company and a company that has been in existence for less than three financial years, may contribute any amount directly to any political party, on obtaining approval from the Board of Directors in their meeting.

Further, the contribution under this section shall not be made except by an account payee cheque drawn on a bank or an account payee bank draft or the use of an electronic clearing system through a bank account. Therefore as per the above provision, DEF Limited cannot contribute 33.75 Crore directly to a political party through a bearer cheque.

As per Section 182 of the Companies Act, 2013; a company, other than a Government company and a company which has been in existence for less than three financial years, may contribute any amount directly or indirectly to any political party. Hence DEF Ltd can contribute any amount to a Political Party.

According to Section 182 of the Companies Act, 2013 Government Companies are not allowed to contribute to the political party. Considering DEF Limited is a Government Company, it cannot make any contribution to a political party even by way of an account payee cheque.

Question 8. Moon Oil Exploration Ltd. (MOEL) was incorporated on 1st June 2007 and the company made a considerable amount of profit in the past years:

- In the current financial year 2019-20, the company wants to contribute to a political party. How much can it contribute?

- If MOEL had contributed to political parties earlier in the year 2017, how much could it have contributed at the maximum during those years?

- The Chairman of MOEL directed its account manager to pay a political party’s office an amount of 50 Lakh by cheque as part of payment to the party, can he do so?

- The Board of Directors authorised a payment to the National Defence Fund too but wanted to not show it in the profit and loss account. Is it possible to do so?

- A sum of 2 lakh was spent by MOEL on an advertisement in a tract published by a political party. How it is to be treated in the accounts of the company?

Answer:

- Under Section 182 of the Companies Act, 2013, a company, other than a Government company and a Company which has been in existence for less than three financial years, may contribute any amount directly or indirectly to any political party.

The Finance Act, 2017 amended Section 182 of the Companies Act, 2013, accordingly the limit on the maximum amount that can be contributed by a company to a political party has been removed. Therefore a company now can contribute any percentage without any limit. - Further, before the amendment to Section 182 by the Finance Act, 2017, the limit of contribution to political parties was 7.5% of the average net profits during the three immediately preceding financial years. Thus, earlier to 2017, it could have contributed only 7.5% of average net profits at the maximum.

- As per Section 182(1) of the Companies Act, 2013, the contribution must be authorized by the board in its meeting by resolution and such resolution shall be deemed to be the justification in law for making such a contribution.

- Section 182(3A) of the Companies Act, 2013, further, contribution under this section shall not be made except by an account payee cheque drawn on a bank or an account payee bank draft or use of an electronic clearing system through a bank account.

- Therefore, the chairman cannot direct the payment to be made unless he is duly authorized by a Board resolution passed at a meeting and the payment is to be made through an Account Payee Cheque/Bank Draft or an electronic clearing system only.

- Section 183 of the Companies Act, 2013 the Board is authorized to contribute such amount as it thinks fit the National Defence Fund or any other fund approved by the Government for National Defence.

- Further, the company is required to disclose in its profit and loss account the total amount or amounts contributed by it during the financial year. Therefore, it is not possible to avoid the disclosure in the Profit and Loss Account about the amount of the contribution made to the National Defence Fund.

- If the expenditure incurred on advertisement in any publication souvenir, brochure, tract, pamphlet, or the like is deemed as a political contribution if such publication is by or on behalf of a political party or if not, then for the advantage to such political party for a political purpose. Therefore, this amount is to be treated as a political contribution and shown in the profit and loss account under the head political contribution. -Space to write important points for revision

Board Constitution Under Companies Act 2013

Question 9. Warner Ltd. is an Indian company with a net profit of 24, 7, 6, and 7 crores respectively in the last four years. Net profit for each of the last four years included a dividend of 1 crore received from WB Ltd. which is an Indian company. Discuss whether Warner Ltd. is required to spend on CSR activities. If yes, how much it should cost? If no, state the reasons for it.

Answer:

Under Section 135 of the Companies Act 2013, the CSR provision applies to companies that fulfill any of the following criteria during the immediately preceding financial year:

- Companies having a net worth of rupees five hundred crore or more, or

- Companies having a turnover of rupees one thousand crore or more or

- Companies having a net profit of rupees five crore or more

Explanation to Section 135 provides that for this section “net profit” shall not include such sums as may be prescribed and shall be calculated by the provisions of Section 198.

Section 198 of the Companies Act, 2013 read with CSR Rules has clarified how a company’s net profit will be computed to determine if it fits into the ‘spending’ norm. To determine the ‘net profit’, dividend income received from another Indian Company or profits made by the company from its overseas branches have been excluded. Besides, the 2% CSR is computed as 2% of the average net profits made by the company during the preceding three financial years.

Now, presume that W.B. Ltd. is duly covered under Section 135 Companies Act, 2013 and is also complying with the said provisions, the dividend received by Warner Ltd. from WB Ltd. shall be deducted from the Net Profit of Warner Ltd. to compute “net profit” & “average net profit” for Section 135 of Companies Act, 2013.

Therefore, based on the above assumption, Warner Ltd’s net profit shall be considered as rupees 7 crore minus 1 crore (dividend from another Indian company) = 6 crore in the preceding financial year, hence making it liable to comply with Section 135. It will therefore be required to spend on CSR Activities.

The CSR amount to be spent/created is 2% of 6 crores + 5 crores + 6 crores = 17/3 = 5.67 crore (average profit of the preceding three years) i.e. 2% of 5.67 crore being 11.33 Lakhs.

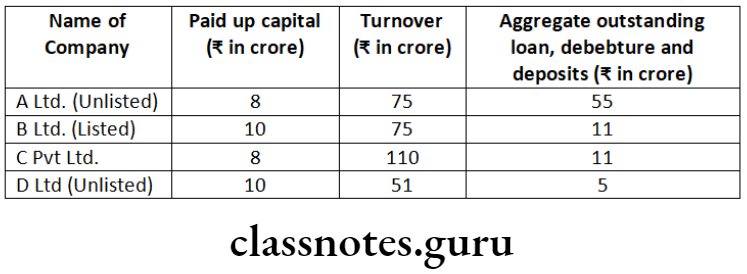

Question 10. RPK Ltd. is an unlisted company having ₹9 crores as paid-up capital and 52 crores as a long term loan. The directors of the company would like to know from you the answers to the following questions:

- Would the company be liable to constitute an audit committee?

- If the company is listed after a fresh issue of shares to the tune of *50 crores, in such a situation, would the company be liable to constitute an Audit Committee?

- What is the quorum for meetings and several meetings to be held in a year by the audit committee?

Answer:

- Under Section 177(1) of the Companies Act, 2013 read with Rule 6 of the Companies (Meetings of the Board and its Powers) Rules, 2014, provides that the Board of Directors of the following companies is required to constitute an Audit Committee of the Board-

- Every listed Public company;

- All Public companies with a paid-up capital of 10 crores rupees or more;

- All Public companies having turnover of 100 crores rupees or more;

- All public companies, having in aggregate, outstanding loans or borrowings or debentures or deposits exceeding 50 crore rupees or more.

Therefore, RPK Ltd. is liable to constitute the audit committee as its long-term loan is more than the prescribed limit of 50 Crore.

- Yes, the company is liable to constitute an audit committee as it will then become a listed company.

- Secretarial Standard-1 provides that the Committee shall meet as often as necessary subject to the minimum number and frequency prescribed by any law or any authority or as stipulated by the board.

Secretarial Standard -1, unless otherwise stipulated in the Act or the Articles or under any other law, the Quorum for meeting of any Committee constituted by the Board shall be as specified by the Board. If no such Quorum is specified, the presence of all the members of any such Committee is necessary to form the Quorum.

Accordingly, RPK Ltd. In the case of unlisted public companies, a minimum number of meetings and quorum may be decided by the Board of Directors.

Question 11. X Ltd. is a listed company having 565 shareholders as of 31st December 2019. The Board of Directors asks you about the formation of the Stakeholders Relationship Committee. Is it necessary to constitute a Stakeholders Relationship Committee? Will your answer be the same if X Ltd. is an unlisted company? What should be the composition of this committee?

Answer:

Section 178- Stakeholders Relationship Committee:

Section 178(5) of the Companies Act, 2013 provides for the constitution of the stakeholder’s relationship committee. The Board of Directors of a companythath consists of more than 1000 shareholders, debenture-holders, deposit holders, and any other security holders at any time during a financial year shall constitute a Stakeholders Relationship Committee.

Section 178(8) provides that in case of any contravention of the provisions of section 177 and section 178, the company shall be liable to a penalty of five lakh rupees and every officer of the company who is in default shall be liable to a penalty of one lakh rupees.

Conclusion: Considering the above provisions, we can state that it is not necessary to constitute a Stakeholders Relationships Committee, in the case of X Ltd. The answer would remain the same even if it is an unlisted Company (both answers assuming that there is no one else except 565 shareholders given in the question)

Constitution of Stakeholders Relationship Committee The Stakeholders Relationship Committee shall consist of a chairperson who shall be a non-executive director and such other members as may be decided by the Board.

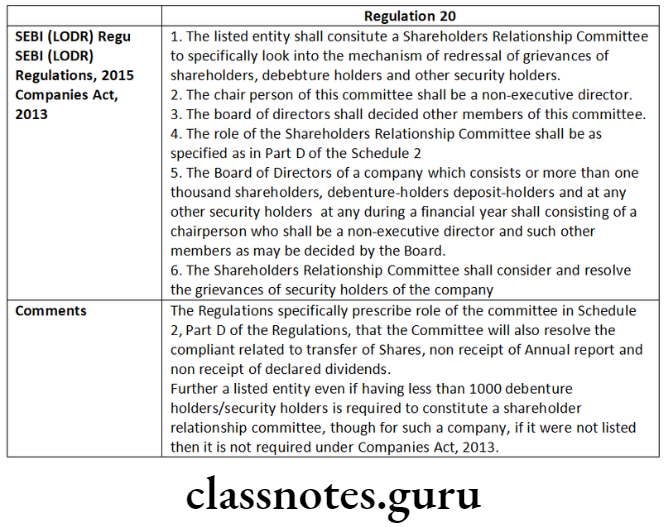

Under Regulation 20 of SEBI (LODR) [Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements)] Regulations, 2015

The listed entity shall constitute a Stakeholders Relationship Committee to specifically look into various aspects of interest of shareholders, debenture holders, and other security holders.

It shall consist of:

- At least 3 directors, with at least 1 being an independent director, who shall be the members of the Committee

- In the case of a listed entity having outstanding SR equity shares, at least two-thirds of the Stakeholders Relationship Committee shall comprise independent directors.

- The chairperson of this committee shall be a non-executive director.

Conclusion:

In the above case, a listed company even if having less than 1000 shareholders is required to constitute a Stakeholder Relationship Committee. In case X Ltd. is an unlisted company, it is not required to constitute a Stakeholder Relationship Committee under the Companies Act, 2013.

As per SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, at least three directors, with at least one being an independent director, shall be members of the Committee.

Powers Of Board Of Directors In Company Law

Question 12. With the scenarios described below, examine whether any of the following companies is required to constitute an Audit Committee as per provisions of the Companies Act, 2013.

Board Constitution And Its Powers Descriptive Questions

Question 1. Explain the provisions relating to the constitution of the Nomination and Remuneration Committee.

Answer:

The Nomination and Remuneration Committee helps the Board of Directors in the preparations relating to the election of members of the Board of Directors, and in handling matters within its scope of responsibility that relate to the conditions of employment and remuneration of senior management, and management’s and personnel’s remuneration and incentive schemes.

The responsibilities of the Nomination and Remuneration Committee are defined in the Nomination and Remuneration policy or terms of reference of the Nomination and Remuneration document.

The Board of Directors of the following companies shall constitute the Nomination and Remuneration Committee of the Board:

- Every listed Public Companies; or

- The following class of companies –

- all public companies with a paid-up capital of ten crore rupees or more;

- all public companies having a turnover of one hundred crore rupees or more;

- all public companies, having in aggregate, outstanding loans or borrowings or debentures or deposits exceeding fifty crore rupees or more.

The following classes of unlisted public companies shall not be covered for the above purpose:-

- a joint venture;

- a wholly owned subsidiary; and

- a dormant company as defined under section 455 of the Act.

The committee shall consist of three or more non-executive directors out of which not less than one-half shall be independent directors.

The chairperson of the company may be appointed as a member, but shall not chair such committee.

Additionally, for listed Companies, SEBI (LODR) Reg, 2015 provides that the nomination and remuneration committee shall comprise at least three directors. All directors of the committee shall be non-executive directors, and at least fifty percent of the directors shall be independent directors.

The Chairperson of the nomination and remuneration committee shall be an independent director. The chairperson of the listed entity, whether executive or non-executive, may be appointed as a member of the Nomination and Remuneration Committee but shall not chair such Committee.

The Chairperson of the nomination and remuneration committee may be present at the annual general meeting, to answer the shareholders’ queries; however, it shall be up to the chairperson to decide who shall answer the queries.

Question 2. Explain the provisions relating to the constitution of the Stakeholders and Relationship Committee.

Answer:

Stakeholders Relationship Committee

Section 178(5) of the Companies Act, 2013 provides for the constitution of the stakeholder’s relationship committee.

The Board of a company that has more than one thousand shareholders, debenture-holders, deposit-holders, and any other security holders at any time during a financial year is required to constitute a Stakeholders Relationship Committee consisting of a chairperson who shall be a non-executive director and such other members as may be decided by the Board.

The stakeholder’s relationship committee shall consider and resolve the grievances of security holders of the company. The Committee shall consider and resolve the grievances of the security holders of the listed entity including complaints related to transfer of shares, non-receipt of annual report, and non-receipt of declared dividends.

The chairperson of each of the committees constituted under this section or, in his absence, any other member of the committee authorized by him on this behalf shall attend the general meetings of the company.

Comparison table of Stakeholders and Relationship Committee under Companies Act 2013 and SEBI (LODR) Regulations, 2015